The Bidirectional Charging Study 2026 shows that whilst interest is high, willingness to buy is still low. So far, only one in six electric car drivers sees real added value.

5-Market bidirectional Charging Study 2026: TEchnology is ready, Market not yet

Power2Drive took place again in Munich during the week of 23 June, and bidirectional charging is once again at the center of attention. The perfect moment to bring solid data to the conversation.

For the Bidirectional Charging Study 2026 we surveyed more than 10,000 people across five countries: Germany, the UK, France, the Netherlands and Sweden.

What makes this study unique:

- We covered all three use cases: V2H, V2G, and V2B

- We surveyed BEV drivers, but also in-depth ICE drivers with varying levels of interest in EVs. This enables forecasting.

The result:

The technology is ready, but the market is not quite there yet.

Awareness is higher than expected, but conviction is lacking

Not every driver is a candidate for bidirectional charging in the first place. Those without a private parking space cannot connect their car to the grid at home. Among BEV drivers with a private parking space, around 38% know what bidirectional charging is. Another 34% are at least familiar with the term.

Among ICE drivers, the numbers are lower, as expected. But even here, awareness is higher than anticipated: 20% know the technology, and another 32% say they have heard the term before.

What does this mean for providers?

The industry’s communication efforts have paid off so far. Investing further in pure awareness campaigns is wasted budget. The bottleneck now is conviction, not reach. Providers who align their messaging with the actual decision barriers will have a clear edge.

Interest yes, commitment no

When presented with the basic concept of bidirectional charging, respondents across the five countries initially find the technology attractive: 53% of BEV drivers can imagine using it. Among ICE drivers, the figure is still 22%.

What does this mean for providers?

A word of caution: stated interest alone is not a reliable indicator of purchase intent or business case calculations. Whoever builds their sales and product communication on that “53% interest” is planning for a target group that simply does not exist.

We need to go deeper.

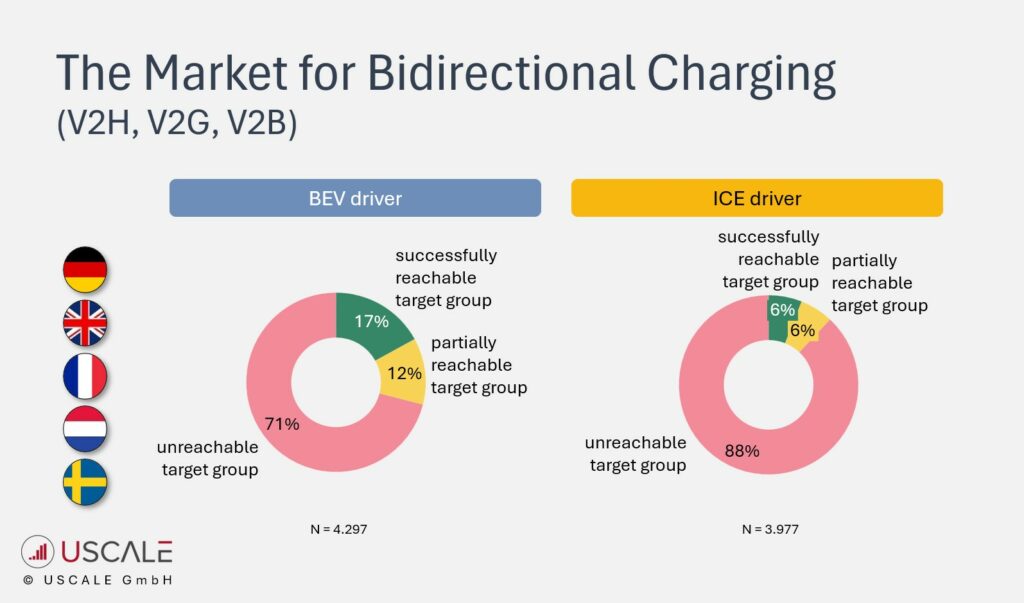

Once respondents weigh the potential pros and cons, opinions shift. Even without knowing the exact investment costs and financial returns, the share of those who see a meaningful personal benefit and would consider investing drops significantly. The realistically addressable target group among BEV drivers falls to 17% on average across the five countries and to 6% among ICE drivers (see chart above).

What does this mean for providers?

These 17% may not represent a huge but very concrete target group. The study shows who they are, what drives them, and how to reach them.

What really motivates

The top usage drivers are expected cost savings, enthusiasm for technological innovation, and environmental benefit. For Vehicle-to-Home, perceived energy independence and the ability to use self-generated solar power are also strong motivators.

For providers, these findings offer a clear foundation on which to build compelling marketing arguments.

What does this mean for providers?

The study provides a clear ranking of motivations for each of the five countries, with direct implications for campaigns and product communication.

The drawbacks carry real weight

Understanding the UK public charging market is only the first step. The next step is understanding your customers. For providers who want to Real barriers stand alongside the benefits. The biggest obstacle is the upfront investment in home charging infrastructure. Add to that concerns about potential battery degradation, uncertainty around a technology still perceived as immature, and a day-to-day effort that feels too high.

Bundled offers from OEMs and technology partners combining vehicle, charging infrastructure, and warranties can partially address these concerns. Until broad trust is established, education remains a core responsibility for all players in the market.

What does this mean for providers?

The investment barrier is the single biggest obstacle. Financing models, all-inclusive packages, or pilot programs with a guaranteed return can move the needle more than any awareness campaign. The study shows which barriers are strongest in which country markets and which offer combinations most effectively increase willingness to pay.

Willingness to invest and revenue expectations

Willingness to invest in V2X is limited. Not every interested party is prepared to spend four-figure sums on a wallbox, retrofit, or hardware. At the same time, revenue expectations vary considerably: what some users consider an attractive return is simply not enough for others to justify the effort.

What does this mean for providers?

The specific financial offer determines whether interest converts to purchase. The study shows, for various price points and revenue promises, how large the addressable target group actually is. A price-volume curve as a basis for pricing and business model development.

Differences across countries and use cases

Conditions, attitudes, and market potential differ significantly by country. Awareness, interest, and the relative weight of individual drivers and barriers vary considerably across Germany, the UK, France, the Netherlands, and Sweden. Clear differences in market potential also emerge between the three use cases Vehicle-to-Grid, Vehicle-to-Home and Vehicle-to-Building.

What does this mean for providers?

One-size-fits-all does not work here. Thinking European but acting with a uniform strategy leaves potential on the table. The study shows which use case has the greatest potential in which market and what matters most when entering each country.

About the study

For the Bidirectional Charging Study 2026, USCALE surveyed more than 11,000 people in February 2026 across Germany, the UK, France, the Netherlands, and Sweden (more than 800 BEV drivers and more than 1,200 ICE drivers as a reference group per country).

Study focus areas:

- Vehicle-to-Home, Vehicle-to-Grid, and Vehicle-to-Building

- Awareness and attitudes

- technical and personal readiness

- Product-Market-Fit

- Willingness to pay

- Revenue expectations

- Purchase and integration requirements

For the addressable target group, the product-market fit was calculated using the Pain-Gain approach (link to methodology).

Your benefit from the study

If you’d like to understand how to successfully develop and market your Bidi offering, do get in touch. In 20 minutes, I’ll show you which insights are particularly relevant to you.

More information about the study, including a full list of contents, is available on our website.

USCALE supports you with data, studies, and insights – as a multi-client study or a tailored ad-hoc study for your specific questions.

Feel free to also take a look at the overview of our multi‑client charging studies!

Contact us now

Which customer insights on electric cars, charging technology, or charging services are you looking for? Whatever you’re searching for, we look forward to exchanging ideas with you.

* mandatory